|

A Trilogy by Bruce Beach

As discussed in the first presentation - The Meaning of Money - money today is most usually 'blips'. Blips are either marks in accounting books or electrons in a computer. In this sense, money may sound all very nebulous. Some people insist that money be 'backed' by gold or silver - but here we will have none of that. A mere scarcity of gold in a community does not mean that the community should not have money. While in the first presentation we went to some length to explain that money is a poor way to store wealth we nevertheless did not disparage the need for money. Money is as essential to a vibrant and vital economic system as is air to an animal. However, one must keep it in perspective. It is not the end-all or purpose of life as unfortunately so many people presently make it out to be. Money is a serious matter. But it is not THAT serious. There is no one system that is best or perfect. There is always a better way. Compare it to paint for a house. Yes, the house needs paint - but there are possible many different colors. Eventually the present or new paint will wear out. There is no reason that it has to be repainted the same color. And yes there are differences between paints. Some are better and last longer than others. But beware of those who say a money system has to be this way or that. Fiat money systems are much better in many ways than metal based systems. Yes, they grow old, decline, wear out - but then also so do all human systems. The real issue then becomes how easily and quickly a new and better working system can be installed. There have been a few successful experiments with alternate money systems. One is the Swiss WIR system.

What we are going to discuss are the simple methods by which any group - from 50 persons to fifty million persons can create money. Our greater focus will be on those systems suitable up to a few thousand people. Beyond that number there will surely be enough people around that understand the principles of bookkeeping and / computers (if computers are available) to set up suitable systems. The first point of focus should be on the immediate local community. The principles developed here can be applied by higher communities which are simply communities of communities rather than communities of individuals. The first step is to make a list of every person in the community that is elegible to have an account. This should at least be every person over the age of fifteen. The individual accounts can be flagged in various ways and it may be desirable for anyone in business to have two accounts, a personal account and a business account, or even more than one business account. How accounts will be flagged will be determined by the bank administration and in my ideal world of Progressive Democracy the bank administrators are appointed and removed at the pleasure of the Community Servants. Some ways in which accounts might be flagged would be:

B - business C - child (until age 15) D - dependent - someone needing supervision E - exceptional - an account requiring exceptional monitoring

The above are only examples of how accounts might be assigned. There could be thousands of variations all depending upon the principles that the community authorities wish to implement, but to understand the suggested principles let us examine the accounts in the example. Accounts 001 and 002 would be accounts for the local community. There could be dozens of community accounts - or if desired only a single community account and internal accounting kept in separate community books. The same would apply to a business that might keep dozens of separate accounts within the internal bookkeeping of that business. Even an individual may keep their own budgetary and internal bookkeeping system. Accounts 003 and 004 reflect the distinction between a personal and a business account maintained by an individual. Accounts 005 and 006 do much the same but have the distinction that account 006 is a privileged account in that it is permitted to receive ear-marked school funds. As an example of how that might happen - the community might deposit to each child's account a set amount of funds and these could only be transferred from that account to a teacher's account. We see an example in accounts 007 and 008 where Tommy Brown might be old enough to have his own adult account but at the same time may be young enough that payments from his child account have to be countersigned by his parents. It is this way that parents would have control over the selection of their children's teachers and consequently over the teaching that their children received. Account 009 is an example of a person that needs a supervised account. They might be a person who is mentally retarded or otherwise incapacitated. In this case it would be their guardian or trustee that had signing or required countersigning authority. This could apply to very elderly individuals who required custodial care - or even individuals that the community decided were irresponsible or incapable of managing community funds that were assigned to them. These have just been examples of how accounts might be set up or designated - but a community may take an entirely different approach. The emphasis here is mainly on an example, one example, of how the mechanics of bookkeeping might be set up. Once accounts have been set up - there are two more issues. The determination of entitlement to community contributions to the accounts and the mechanics of transfers between the accounts. The first of these issues is so important that it is dealt with on its own web page called Money Matters and in the remainder of this page we shall only deal with the mechanics of transfers. The method of transferring money from one account to another is very simple. All that one does is write a check.

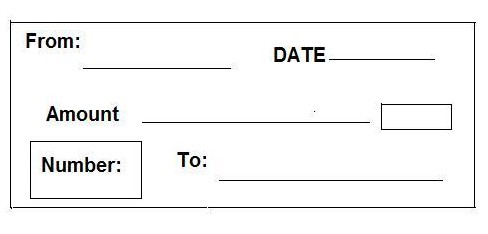

and their account number on the community list.

Date: is the date they issue the check

Amount: Is the amount of the check

To: is the name of the person

Number: is the transaction number

People, if they wish, may give receipts for the currency that they receive - and those making a deposit of the currency may keep a deposit slip record of what they have deposited. Any individual can implement any system of controls that they wish and in order to simplify the system for others people might issue the checks / currency / money in accepted denominations just as currency today is kept in specific denominations. Therefore, the issuing person, in order to pay a $36.30 bill might either write out checks for $20, $5, and $1 and even thirty cents - or they could write a check for the entire amount - or they might have checks from others in their pocket that in some combination would add up to the amount. A community might also make substitutes for coins. The proverbial wooden nickels in any denominations and these could be 'sold' by the bank, so that exchanges for small amounts could be handled by using these tokens made of wood, plastic, metal or what have you. There could also be bank issued checks / money / currency of various denominations that one might obtain from the bank by writing a check to the bank. As technology might permit these could be more fancily printed. One considered factor, however, is that they might be dated so as to become invalid after a certain date for reasons such as will be discussed in Money Matters. These are all just the mechanics of creating money and keeping track of it. There is nothing, or needs to be nothing, really that complicated about the procedure. The purpose of this money is simply to keep track of transactions within a small community where everyone is known to each other and there should be little difficulty in determining the culprit if someone should try to defraud the system. As has been repeatedly stated - the greater issue is one of entitlement - and that shall be covered in Money Matters. Here we are only concerned with an elementary tracking system. When the checks / currency / money (the terms are in essence synonymous and are all referring to the same piece(s) of paper) are presented to the bank they are then assigned a transaction number which is written onto the check and the check can then be filed with all the others in that order. The order in which the checks are entered into the transaction register has nothing to do with the order in which they are written but only the order in which they are presented to the bank.

The above is a random example out of a transaction register showing the four transactions from 811 to 814. Each transaction has both an issuer and a depositor although, as explained above, the depositor may be a different account than to which the issuer originally gave the check.

Here we see one Individual Account Register that happens to have been affected by two of the above transactions on the Community Transaction Register, specifically transactions 811 and 814. All entries on an individual account appear as either a receipt or a payment - but not both.

2. Then in transaction 811 he paid out $130 to account 076. This put Charlie Champ in an over-draft situation of $30.00. 3. Following this Charlie Champ received $70 from account 025 and so had a balance of $40.00. 4. And finally in this series of transactions for Charlie Champ he paid out $15 to account 004 and so had a balance of $25.00.

The accounting procedure is not time sensitive and it makes no difference whether individual accounts are in over-draft or not. There just needs to be account reconciliation on a timely basis as decided by the system managers and the subject of the relative importance of account balances is something that will be discussed under Money Matters. In this presentation we have only been concerned with the mechanics of accounting in the process of money creation. It is not a complicated matter and most any community will find someone who can manage these details.

|